Summary views

- Synergy primarily makes wind castings (85% of revenue).

- We believe Synergy Green can grow topline at mid to high teens over long periods of time (wind is a growing industry, + 1 tailwinds exist and there is a sizeable non wind opportunity).

- This should translate to bottom line >20% CAGR as margins improve over time (more inhouse machining, solar cost savings, operating leverage).

- Synergy Green is gaining market share with marquee customers in its core business (wind castings) which has high entry barriers (technology edge, consolidated industry structure) and we see roadmap to steady state 18%+ ROE with moderate debt over time.

- Company is run by fanatic promoters that inspire deep trust (clear vision backed by strong execution track record, granular thinking, deep domain expertise and ethical reputation) and whose focussed strategy we are aligned with.

- Trailing valuations are misleading as the company is in a massive investment phase while P&L metrics are not steady state due to expense impact, however normalized valuations are reasonable (~23x normalized PE1FY26e) given scope for earnings longevity (casting industry is sizeable, Synergy can expand its scope of manufacturing activities)2

- We see meaningful opportunity for value creation over time as Synergy Green is a high quality scalable business that is relatively undiscovered today with limited institutional shareholders and no sell side research coverage.

We have initiated a ~4% position weight in Prudence and 6% in the Microcap AIF and may use further price or time corrections to increase our position size.

What do they do?

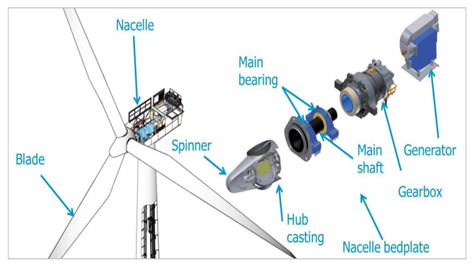

Synergy Green is a leading supplier of high value, critical, large SG iron3 castings (up to 30 MT in size) primarily for the wind industry (~85% of sales) with the balance spread across various industries (mining, plastic injection, pumps, automobile dies, power etc).

Wind casting process involves melting of scrap iron in induction furnaces, then chemically treated with magnesium, which is then poured into a sand mould shaped like the finished component and left to solidify. Once cooled, the sand is broken away, the casting is cleaned and tested for internal defects before being precision-machined and assembled into wind turbine.

Their product portfolio is comprehensive (~97% of wind castings covered) and includes in wind turbine (rotor hub, main frame, main bearing housing, shafts etc), wind gearbox (torque arm, housing & planet carrier etc) and non-wind (mining frames, plastic injection clamp cylinders & platens, pump casing & diffusers, compressor cylinder, automobile dies etc.)

In a later section, we explain what these products do and why they are complex to make and have high entry barriers.

Synergy Green makes the following products.

Wind castings for turbine and gearbox (~85% of sales) and non wind castings (~15% of sales)

Brief history of Synergy Green

- Synergy Green was incorporated in 2010. It was co-promoted by the Shirgaokar group and Mr V Srinivasa Reddy.

- Synergy is part of the 100+ years old Shirgaokar group led by Mr Sachin Shirgaokar which has diverse business interests across the sugar, foundry, general engineering, IT & hospitality sectors and so has benefited from the broader group’s engineering expertise. Co-founder Mr V Srinivasa Reddy is the professional technocrat who brings strong foundry expertise 4(B.Tech Mechanical engineering, M.Tech in foundry tech from NIFFT and over 30 years+ work experience in castings with ISGEC, Simplex Castings and L&T where he was instrumental in turnaround and scale up of L&Ts foundry business).

- They set up a greenfield foundry in Kolhapur in 2011 with a foundry capacity of ~12,000 MTPA. As a new entrant competing with established giants (Suzlon, L&T), Synergy faced challenges in establishing customer credentials during early years. However, by 2013 they were able to onboard marquee customers such as Siemens Gamesa, Vestas and GE. Company has been a supplier to the non-wind segment since its inception with clients such as Terex Corp with whom they enjoy dominant wallet share.

- Synergy raised ~26 Cr Equity via an IPO in 2018 which allowed it to further expand capacities to 30,000 MTPA in 2019. In the same year, Synergy forayed into the more profitable export markets by supplying to Vestas globally.

- Over time Synergy has strengthened its technical competencies. Initially focusing on smaller wind turbine castings, company was the first Indian player to adopt semi automated fast loop moulding lines 5 capable of producing large parts up to 30 MT. Company has now evolved into an end to end solution provider by foraying into in house machining which earlier was 100% outsourced due to capital constraints.

- In the last few years, Synergy has been able to onboard multiple large customers (Envision, Nordex, Adani Wind, Senvion, Mahindra, L&T etc). Within 15 years of incorporation, Synergy has achieved reasonable market share in wind castings (~20% share6).

- Backed by marquee new customer additions, technical progress and ~46 Cr equity raise via rights issue in 2024 Synergy has further expanded its foundry capacities to 45,000 MTPA in 2026. In the past 2 years Synergy is doing more capex than it did cumulatively since inception, reflecting promoter confidence in future growth prospects.

- In the last few years, the next gen promoters (Shreya Shirgaokar and Manasa Reddy) have also fully joined the business.

Synergy Green has demonstrated strong growth over long periods of time despite headwinds

Strong growth demonstrated over long periods is remarkable given the multiple growth headwinds faced over the years.

- Regulatory impact from unfavourable tariff change in India7 in 2017 and uncertainty around accelerated depreciation tax benefit in 2012.

- Challenges faced by major customers in the past like Vestas global being impacted by Ukraine war, Siemens Gamesa India losing market share8 or Enercon India shutting down.

- Significant commodity price inflation post Covid (input prices went up by 30-100% 9during FY21-22 period).

- Tepid growth over last few years due to capacity constraints (between FY24-26, avg capacity utilisation was at peak levels of ~85% on 30,000 MTPA).

Source: Ace Equity

Growth has been accompanied by improvement in earnings quality, resilience in business model.

- Customer concentration has meaningfully reduced over time with largest customer accounting for < 25% of sales.

- Since foraying into exports in FY19, Synergy now is more geographically diversified as share of margin accretive exports (direct castings + indirect via domestic OEM) now accounts for ~40% of sales.

- Synergy increasingly focused on larger, complex products (lower competition) evolving from castings for 2 MW turbines to 5 MW turbines.

- While revenues from wind industry is meaningful share at present (~85% of sales), that is deliberate strategy. Wind is a growing industry where Synergy has strong right to win and customer demand visibility. We believe they could further diversify into other industries over time.

- Despite high concentration in wind industry which has faced headwinds in the past, Synergy has never seen EBITDA degrowth barring 1 year since turning profitable in FY15.

- Balance sheet resilience has improved as the Net debt/EBITDA has improved from ~8.3x in FY15 to <2x in FY25. At present it is at ~4x as production costs from expanded facilities have hit the P&L however this should improve as revenues flow through over time. We believe brief periods of high debt in capital intensive businesses is par for the course and something we are willing to live with as the only other alternative is slower growth or significant premature equity dilution both of which impacts us as long-term shareholders.

Business evolution over time

| Particulars | Decade back | At present |

| End industries | Wind turbine (few customers) Wind gear box- single customer General engineering (non wind) mining & pump Industry | Now with top 5/10 wind OEMs globally and all major OEMs in India. Top 2 wind gear box players (~45% of global market) 10 Within non wind expanded into all major repetitive large casting industries like plastic injection, power sector & automobile dies |

| Key customers logos | Vestas, Siemens Gamesa & GE in wind turbine ZF for wind gear box Terex non wind | + Nordex, Adani, Envision, Senvion (wind turbine) + Flender (gear box) BHEL, Mahindra, L&T, Ferromatic Milacron, Wilo (non wind) |

| Product range | Casting Sizes up to 17 T catering up to 2 MW turbines | Enhanced capability to produce larger and complex castings up to 30 MT and catering up to 5 MW turbines |

| New competencies Developed | Castings | Castings + Machining & surface treatment + Captive renewables |

| Capacity /Gross Fixed assets | 12,000 MT – Foundry Gross block- 55 Cr | 45,000 MTPA – Foundry 20,000 MTPA – Machining 10 MW captive solar (15,000 TPA) Gross block -260 Cr |

| Customer concentration | High customer concentration Vestas – 60% of sales during Covid | Well diversified customer base No customer > 25% of sales |

| Geography Mix | Largely domestic sales | ~40% of Sales from exports Direct exports spread across USA, Europe, Australia etc |

Business evolution has translated to better economics over time

| Key financial metrics | FY15 | FY19 | FY25 | Comments |

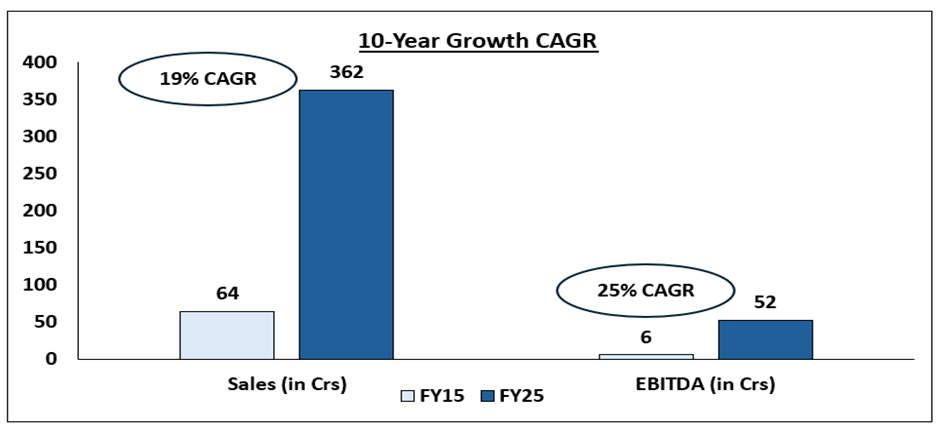

| Sales | 64 | 165 | 362 | |

| Gross margin (%) | 54% | 66% | 61% | Operating leverage with larger scale Better mix (exports, larger, complex parts) Availed early payment discounts |

| EBITDA margin (%) | 9% | 12% | 14% | |

| Net profit margin (%) | -11% | 3% | 5% | |

| ROIC (%) (Pre tax) | -2% | 19% | 22% | |

| ROE (%) (Post tax) | N/A | 12% | 16% | |

| Inventory days | 94 | 106 | 54 | Better efficiencies with scale and better customer mix |

| Debtors days | 65 | 65 | 57 | Bill discounting |

| Creditors Days | 130 | 114 | 60 | Availed early payment discounts |

| Other days | -17 | 12 | 0 | |

| Working capital days | 13 | 69 | 51 | |

| Net Debt EBITDA ratio (x) | 8.30 | 1.86 | 1.94 | |

| GFA turns | 1.28 | 2.21 | 1.76 | Better utilisation levels Historic expansion via brownfield |

| NFA turns | 1.94 | 5.03 | 3.62 |

Synergy Green is very well positioned for sustainable growth over long periods of time

Synergy Green can grow its topline at mid to high teens and profits >20% CAGR for very long periods of time as:

- Wind industry in India and globally is a growing market as it enjoys sustainability tailwinds and is seeing demand from both government and industrial users.

- Synergy is competitively positioned vs domestic peers and should be a beneficiary of + 1 tailwinds (China and Europe) both in India and globally as West lacks manufacturing cost competitiveness and supply chain derisking from China is a strategic priority for MNCs.

- Technical skillsets and capacities are fungible and there exists a sizeable non wind castings market in which Synergy is at early stages of growth. As non-wind segments increase as % of total, there will be more resilience from any sectoral headwinds.

- We see scope for faster profit growth through margin expansion as multiple levers exist (in house machining, solar cost savings, operating leverage).

Wind industry is a growing opportunity and is complementary to solar

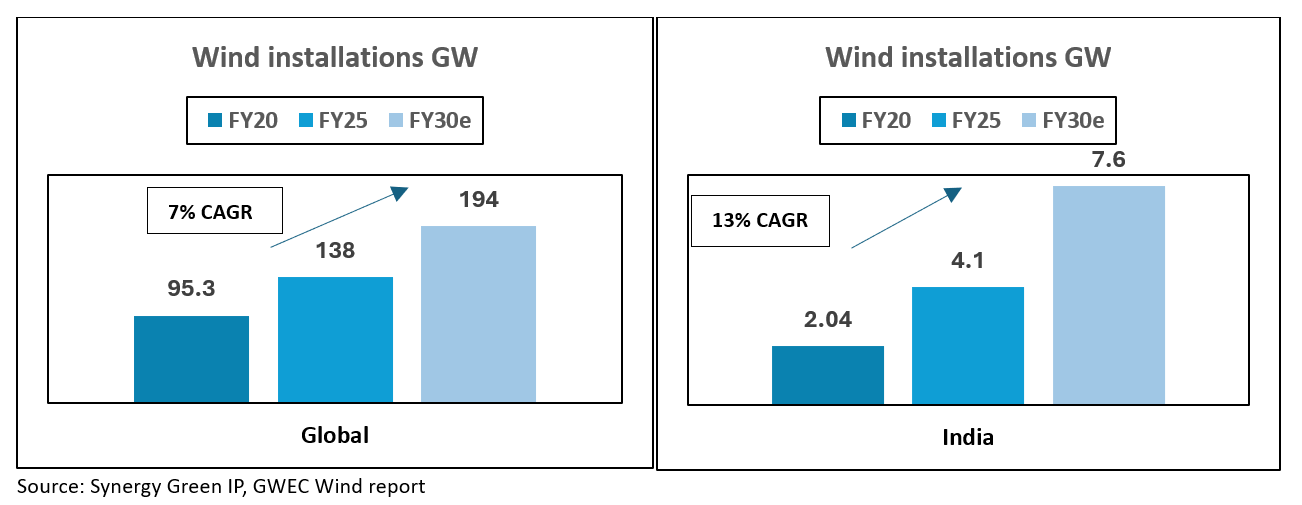

The global wind castings is a large opportunity at 1.5Mn T p.a. 11growing at ~9-10% CAGR due to rising demand for wind and need for more castings as size of turbines became larger.

We broadly estimate the demand for castings globally and India in CY 2026 to be ~25,000 Cr and ~3,000 Cr12 which presents a sizeable opportunity given Synergy’s current scale.

Wind energy is one of the cleanest energy sources (doesn’t emit carbon, NOx or Sox, consumes negligible water or fuel), and is playing a crucial role in net zero commitments/climate goals as specified in the Paris treaty agreement13. Additionally, the need to localize energy security has been strong imperative for leading economies (Europe high dependence on Russian gas got exposed post Ukraine war, India remains dependent on imports for crude oil which is being tested due to ongoing Middle East tension etc.) There also exists strong industrial demand as many corporates (Apple, Microsoft, Google, Amazon, TATA etc) have pledged to get to 100% renewable energy in the long run.

While China still dominates the wind industry (>70% of new global installations) there has been progress made in other regions. Wind now accounts for ~20% of EU electricity supply (2nd largest energy source) with an ambitious target of ~35% by 2030. 14 There exists strong corporate interest with 50% share of new PPAs in EU signed for wind power. While the new US presidency has created some uncertainty around wind policy15, wind still accounts for ~10% of US electricity due to its cost competitiveness and will be a beneficiary of fast growing opportunities such as data centers, cloud computing etc.

India has the 4th largest wind installations in the world and has only scratched the surface in terms of penetration. Despite wind industry facing multiple challenges in the past decade (land acquisition difficulties, grid evacuation etc) sector has grown ~9-10% CAGR to ~55 GW installed capacity today. Situation today is more favourable with 2025 seeing record additions (~2x additions of 2023) and supportive govt policy (wind specific RPO16 for discoms, ISTS charge waiver, accelerated depreciation benefit etc). There also exists strong industrial user demand for wind contributing 60-70% of new additions in 2025.17

While the solar industry (~140 GW installed) has historically outpaced the wind industry, we see both as complimentary given hybrid (solar + wind) is essential to provide round the clock power (solar generates power during the day, wind in the evenings/night and are seasonally complementary) and is currently seeing strong demand (~45% 18of RE tenders are for hybrid). We are seeing initial efforts to rebalance equation with Maharashtra govt incentivizing wind generation while penalizing solar19. We believe battery energy storage systems (BESS) will play a greater role over time however, they will not replace wind. Solar + wind, backed by BESS will co-exist in hybrid projects. Today wind + solar hybrid tariffs are cost competitive at Rs 3-3.5/-unit versus solar + BESS at 4.3-5/- unit and there is no replacement for wind in long duration coverage20 in a day, power generation during monsoons.

Synergy Green is competitively positioned within the large & growing wind casting opportunity

Indian casting players are well positioned to gain market share

We believe there exists a global opportunity for domestic wind casting players as MNCs looks to derisk their high dependence from China and given Europe faces structural issues (high cost, strict regulations).

- At a time when geopolitical tensions between the West and China are rising, MNC derisking their high dependence on China (account for 70-80% 21of global wind castings) is of strategic importance. While China has historically enjoyed meaningful cost advantage (15-30%) due to lower commodity prices, incentivised power costs, larger scale advantage, subsidies etc. We expect their edge to narrow due to a relative increase in labour costs,22 INR depreciation versus RMB, US imposition of tariffs on China (25% under Section 301) while also deeming them an entity of foreign concern whereas Europe has imposed anti-dumping duties and is investigating unfair Chinese subsidies.

- In India, the share of Chinese wind casting imports has structurally reduced to ~20-30% due to stringent regulations imposed (Indigenisation push from ALMM,23 ~8-10% custom duty and BIS certification) which has almost eliminated the cost advantage China historically enjoyed.

- Manufacturing in the West remains quite uncompetitive. Europe (~10% of share) suffers major cost disadvantage (25-30%+ difference) due to high labour & power costs and strict environmental compliance rules which makes manufacturing unviable, which has resulted in shutdowns of foundries including that of Baettr24. USA has a negligible manufacturing footprint today and relies heavily on imports.

India has an established ecosystem in place (India is the 2nd largest casting producer globally and holds 5-10% share in wind castings) and is well positioned to capture this opportunity. Additionally Indian wind casting players can benefit from global wind OEMs (Vestas, Nordex) setting up manufacturing in India for global supplies. The recent EU- India FTA and expected reduction in US tariffs from 50% to 18% only enhances Indian player’s competitiveness.

We believe the + 1 opportunity is a structural trend, something other Indian casting cos also highlight.

| Indian casting co | Management commentary |

| Steelcast | Customers, especially in the U.S., increasingly evaluating non-China cost competitive suppliers. As a result, we continue to see healthy engagement and inquiries from U.S. customers. |

| Kirloskar Ferrous | There has been a noticeable increase in inquiries and a strong interest from global customers to develop and source more castings from India, specifically seeing “a lot of interest from the Americas”. |

| Thaai Casting | Won order from Canada-based company that was previously manufacturing these products in China and is now shifting its manufacturing to India. Gear shaping and planetary carrier machining for wind power opportunity was import substitute from China and Germany. |

Within the Indian wind casting landscape we believe Synergy Green is very well positioned to gain share

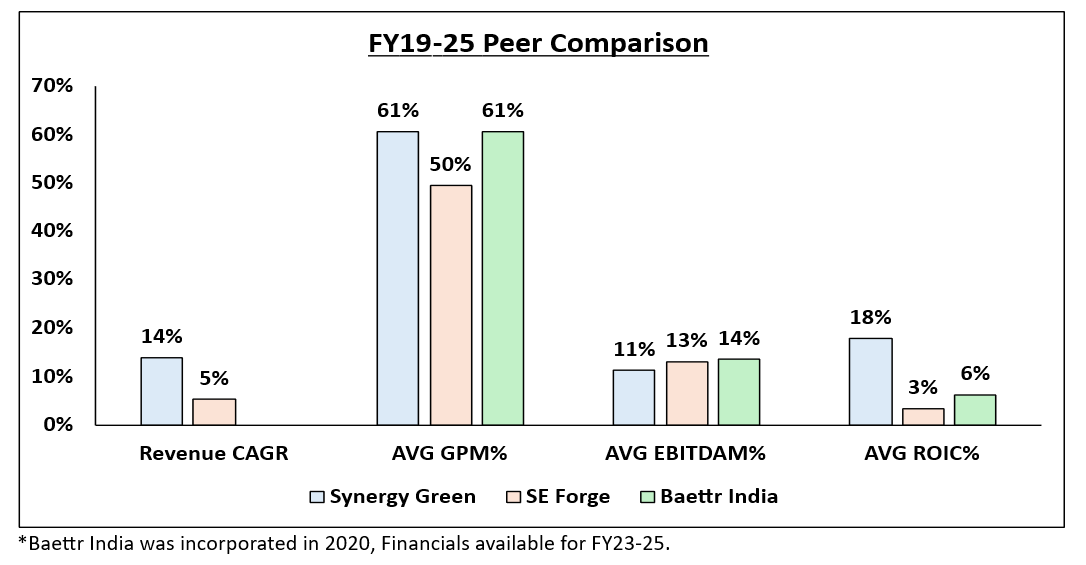

The domestic wind casting in India is consolidated with 3 domestic players (Synergy Green, SE Forge and Baettr). Synergy Green has ~20% market share and is competitively well positioned vs peers to further gain market share for the following reasons.

- Synergy Green is a pure play wind casting co unlike SE Forge (Owned by Suzlon who accounts for a sizeable share of SE Forge’s revenues) and can win customer trust who are more comfortable sharing their product designs. Synergy also enjoys a pricing advantage as SE forge set up is in an SEZ (attracts custom duties, creates ALMM complications) and has been able to sweat its assets more efficiently as reflected in superior ROIC/asset turns25. While SE Forge does 100% machining in house today, we expect this gap to narrow as Synergy intends to do more in house machining.

- Synergy Green enjoys a more diversified customer base unlike Baettr which was formerly part of Vestas and derives large share of sales from them. While Baettr enjoys good quality due its Europe sourced technology, it carries a more expensive cost structure due its MNC profile.

Synergy has demonstrated faster growth, comparable margins and superior ROIC %

We expect Synergy to enhance its cost edge over domestic peers and reduce gap versus China as customer pricing improves with cost benefits from following measures.

| Activity | Cost incurred today % sales | Cost % sales post investment | Potential cost savings % sales |

Comments |

| Machining | ~15% |

~10% (at 50% machining in house) | ~5% | 50% machining will be done in house with 20 K MTPA capacity. ~100 Cr capex over 2 phases. This will reduce costs, lower lead times, offer better quality control and position Synergy as one stop shop solution. While it’s a new, complex technology, Synergy has seen early success in proto typing. |

| Solar (captive) | 8% | 6% | 2% | 30 Cr capex to expand from 2 MW to 10 MW. More sustainable footprint is important for global customers. |

| Foundry | Fixed costs- ~9% | Fixed costs- ~8% | 1-2% Op leverage + bargaining power | 60 Cr investment incurred to expand from 30K MTPA to 45K MTPA. Op leverage due to brownfield expansion, more automation and better RM related bargaining power. |

| Total | ~8-9% |

Note: Solidarity estimates

We remain very confident in company’s wind industry growth prospects as company has made meaningful progress in terms of building credibility with global OEMs (works with 5 of the top 10 global wind OEMs, including Envision the No 2 Chinese OEM) and is also catering to the global demand of some OEMs like Vestas, Nordex etc.

Company enjoys very strong demand visibility with its existing customers with ongoing foundry expansion to 45 K MTPA fully backed by order visibility. Going forward post reaching a healthy utilisation, company intends to further expand capacities (medium term vision is 1 lac MTPA) which we think is doable give the customer interest remains higher than current capacities (~600-700 Cr demand visibility) and there exists a large opportunity outside of wind castings which Synergy can cater to.

Some examples of strong customer interest in wind 26

- Vestas has been a stable anchor customer with whom Synergy’s share of wallet has meaningfully expanded over time through a combination of direct exports to US/Europe or exports via Vestas India plant and we expect to continue growing as they reduce their dependence on China.

- Envision (Chinese OEM) is a large player and while current business is restricted to some wallet share of their 3.3 MW turbines as it’s a relatively new customer, this can further scale up once trust is established. There can be potential opportunities with other Chinese OEMs (Sany, Goldwind) in the future as they look to localize their manufacturing in India.

- Synergy has benefited from Adani’s initiative to import substitute from China for their 3.3 MW turbines.

- Synergy has been successful in developing large castings for Nordex’s 5 and 6 MW platforms which offers a strong export opportunity.

Non wind segment represents a sizeable opportunity in the long run

The large castings non wind segment is a larger market (~6Mn MT 27) compared to wind (~1.5Mn MT) and it’s a segment where Synergy has been present since inception (~15% of sales, marquee customers) and is seeing strong RFQ traction across industries (auto, plastic injection, power, mining etc). Capacities are fungible between wind and non-wind and since wind is technologically more complex, we expect the scale up learning curve in non-wind to be smoother.

Historically Synergy due to limited capacities had prioritized opportunities in the wind segment, which was their forte and where customer base was consolidated (non-wind is highly fragmented requiring more sales efforts), strategy which improved their competitive edge through economies of scale/greater customer wallet share. We see merit in their focused strategy as we believe companies in the early stages of growth must build strong roots (market leadership, scale benefits) before scaling up other verticals. Over time as capacity is no longer a constraint, we expect share of value added non wind segments (higher margin, repeat business) to increase 28which will help diversify revenues.

Synergy business enjoys healthy ROEs backed by favourable industry structure and technology edge.

Synergy operates in a consolidated industry which enjoys high entry barriers.

While there are many casting suppliers in India, large size wind castings enjoy high entry barriers with only 3 serious domestic players today despite many players who entered the space but exited over time. 29

Quality standards are very stringent – parts must withstand extreme dynamic loads and operate at sub-zero temperatures (can go up to -40°C) for up to 25-30 years with no margin for failure.

Such high quality standards mean that rejection rates can be high for a new entrant which is very cost prohibitive given the high value nature of parts. This along with the high capital intensity of the business results in stretched timelines for profitability. For example, SE Forge despite commencing activities in 2008 only turned PAT positive in 2024.

Building a high quality product requires deep expertise in metallurgy & chemistry which can’t be built overnight. Running a foundry is highly complex given multiple variables at play (~2 billion variables with ~150 different RM, ~100 products, ~300 machines, ~300 people) 30 as each part is unique and customised. Additionally, wind castings require no bake foundry process in which chemical recipe is highly sensitive to environmental conditions and requires hourly monitoring/adjusting to changes in temperature/humidity etc.

While castings account for just ~5% of wind turbine material cost, they are critical as any failure can risk the entire machine. Hence winning customer trust is very difficult as qualification processes are long (12-24 months) and it can take many years to get onboarded as a vendor. Once onboarded, switching costs are high given customers share designs, make investments in expensive moulds/patterns.

We believe Synergy Green is in a competitively strong position with healthy market share and deep customer trust31 based on a strong track record of meeting high quality standards, offering cost competitive pricing, ensuring consistent delivery even during tough periods like Covid etc. Synergy remains a preferred vendor for marquee customers due to its complete product portfolio, best in class manufacturing setup, end to end solution offering (post machining foray) and quick support due to local presence.

Synergy’s moat translates to healthy ROE.

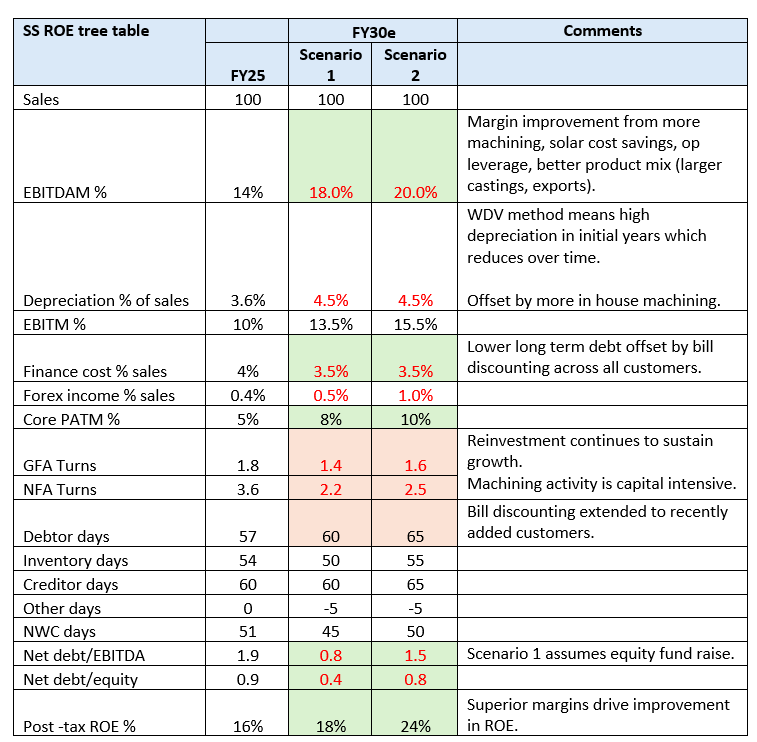

We expect Synergy to generate steady state ~8-10% PATM translating to ~18%+ ROE % with moderate debt which is sustainable given strong technology edge in large wind castings.

- Gross profit margins 32should sustain at 60%+ levels with scope for improvement as share of in house machining increases over time. This should translate to ~18-20% EBITDAM with benefits of solar cost savings, operating leverage and more automation.

- While management focus is growing topline rather than improving margins at present, in the long run we see scope for further improvement in EBITDAM through more machining, better product mix, efficiencies in line with other Indian casting players who do machining in house. (EBITDAM FY25 of AIA Engineering- 27%, Steelcast-28%, Thaai Castings- 24%).

- We expect asset intensity to remain high (GFA turns at ~1.5x and NFA turns at 2.5-3x) as share of capital intensive machining goes up and Synergy continues to invest for growth.

- The Avg. NWC days should remain tight at 40-45 days as Synergy uses bill discounting and inventory days remain tight as more activities are done in house.

We believe our buying price offers reasonable valuations for an initial position

Synergy Green is an attractive business to own given it enjoys strong growth prospects, healthy ROEs backed by favourable industry structure and technology edge, is run by a fanatic promoter with a strong execution track record who inspires deep trust with their ethics/technical competencies.

We believe valuations are attractive for an initial base position. While the reported PE seems expensive at ~100x, we believe that is misleading and not a correct indicator of fair value. For B2B manufacturing cos which are embarking on a large capex program, entry P&L metrics can be misleading as significant costs get upfronted (production costs, depreciation and finance cost) whereas revenues are generated over time. Synergy trades at a normalized PE FY26e of ~23x (basis steady state PATM of ~8-10% versus ~2.5% currently) implying ~17/12x33 EV/EBITDA FY26e/FY27e which we believe is quite attractive for a business that can grow topline at 20%+ CAGR for the next 5 years.

We think the attractive entry valuations can be explained by lack of any institutional coverage, the adverse investor sentiment due to broader microcap selloff and near term earnings disappointment as Synergy’s FY26 guidance is likely to be missed. In the short term, execution delays tend to get amplified in smaller companies as they are not very well diversified. This is all part of the game. Volatility due to short term misses, but where the long term story is intact, is a buying opportunity. We believe well run businesses merit a longer rope and see strong potential for long term Earnings compounding through market share gains, entry into broader castings & expansion into other manufacturing activities over time.

We have initiated a ~4% position weight in Prudence and 6% in the Microcap AIF and would like to add more either on price declines, time correction, or with more evidence of execution.

You can also watch a video of Solidarity’s conversation with Mr Reddy here.

Please click here if you would like to download the PDF version of this blog

- Mcap of ~780 Cr (500/- share price), whereas normalized PAT is ~34 Cr (assuming ~380 Cr Sales FY26 and steady state PATM of ~9%). ↩︎

- Synergy does castings, machining and surface treatment in house. Forgings, fabrication & sub-assemblies remain unexplored today. ↩︎

- Predominantly spheroidal graphite iron but also does grey iron/steel castings. ↩︎

- Awarded Indian foundryman of the year 2024-25 by Indian Institute of Foundrymen. ↩︎

- Mechanised conveyor-based system where large sand moulds move through sequential preparation stations automatically offering better productivity. ↩︎

- Estimates basis ~72 K MTPA India wind castings demand this year (6 GW x 12 K MT per GW) and Synergy’s expected domestic wind castings output of ~15 K MTPA. ↩︎

- Feed in tariffs system got replaced by reverse auction resulting in high competition driving tariffs lower from Rs 5/unit to 2.5-3/unit. ↩︎

- Lost market share to Indian & Chinese players, eventually divested ~90% stake to TPG led consortium in 2025. ↩︎

- Source: Annual report. ↩︎

- Link ↩︎

- Source: Mgmt. estimate. ↩︎

- Assuming 150 GW and ~20 GW installations (Including exports), 160 Cr of castings per GW. Non-China share is ~30-40% within overall global installations. ↩︎

- Paris Agreement aims to limit global warming to 1.5°C. The COP28 target which adopted by ~200 governments aims to triple renewable energy capacity by 2030. ↩︎

- The EU’s 2030 targets are binding under the Renewable Energy Directive. ↩︎

- One Big Beautiful Bill Act reduces timelines for availing credit to 2028 versus Mid 2030s in IRA ↩︎

- ~7% Renewable Purchase Obligation target by March 2030. ↩︎

- Link ↩︎

- Link ↩︎

- MERC had restricted energy banked during solar hours (09:00–17:00) to be drawn in the same ToD slot, however this has been stayed by high court. Additionally, there is 20–30% discounts during solar hours and about 25% surcharges during peak hours which remains in effect. ↩︎

- Upto 4 hour BESS storage is now cost competitive. Beyond that cost doubles with doubling in duration which makes it expensive. ↩︎

- Source: mgmt. estimates verified with customer checks. ↩︎

- Blue collar foundry labour cost is ~3x higher in China, 6x in Europe versus India- Source: mgmt. discussions. ↩︎

- Approved/revised List of models and manufacturers require 70%+ indigenisation levels while capping CKD imports. ↩︎

- ~50% of high-quality German foundries have been forced to shut down over the last decade. Industry expert. Link ↩︎

- In FY25, Synergy generated ~360 Cr sales against ~200 Cr gross block, whereas for SE Forge it was ~490 Cr sales against ~1,100 Cr gross block. Average ROIC over FY19-25 for Synergy was ~18% versus 3% for SE Forge. ↩︎

- Source: concalls, mgmt. discussions ↩︎

- Source: Mgmt. estimate. ↩︎

- Mgmt. long term aspiration is non wind should be ~30-40% of sales. ↩︎

- 15-20 players tried entering in early 2000s but were unsuccessful and had to exit- Q2FY25 Synergy concall ↩︎

- Source: mgmt. discussions. ↩︎

- Feedback basis primary checks done with top customers. ↩︎

- Sales less COGS ↩︎

- Assuming 380/500 Cr Sales and 15/17% EBITDAM in FY26e/FY27e. ↩︎