Perspective on Life Insurance companies post-budget

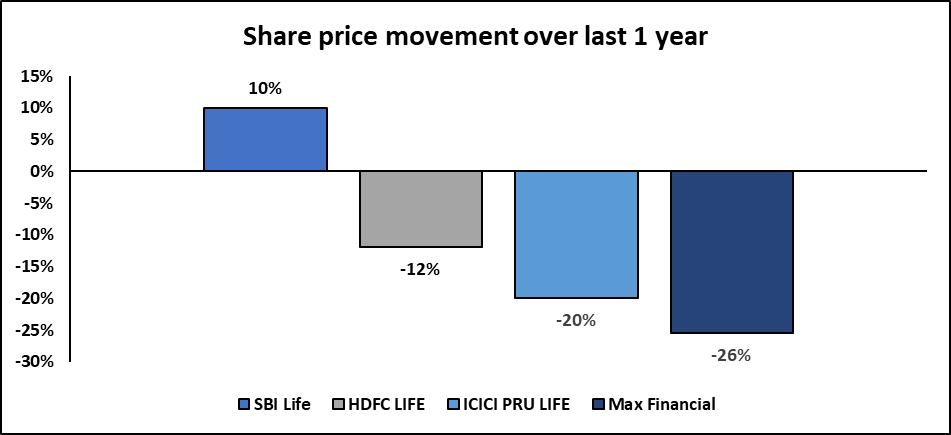

Share price of Life Insurance companies have fallen 8-16% in last 2 days.

Life Insurance companies get almost 25-30% share of their total premiums from long duration savings products which enjoy tax benefits under Section 10 (10D) which make them superior products vs Debt instruments when measured on a post-tax basis.

The budget had 2 announcements with implications for Life Insurance companies:

- Modifications in Section 10 (10D) for premiums over 5 Lacs/year – if the premium paid on Savings policies (excluding ULIPs) exceed INR 5L in a year, then the income earned from those policies will now be taxable (except in case of death benefit).

- The FM signalled intent to nudge individuals to migrate to the new tax regime under which there will be higher exemption limits, but Section 80C tax benefits will be withdrawn.